Feb 26 - Market Building Momentum

- Feb 23

- 3 min read

Steady Pricing, Shifting Activity

For the last three years, home prices have largely held their ground while interest rates have remained elevated compared to the ultra-low pandemic-era. Some see stagnancy. Others see stability. Either way, the market hasn’t been dramatic. However, January may be signaling that momentum is building — and that 2026 could bring meaningful change.

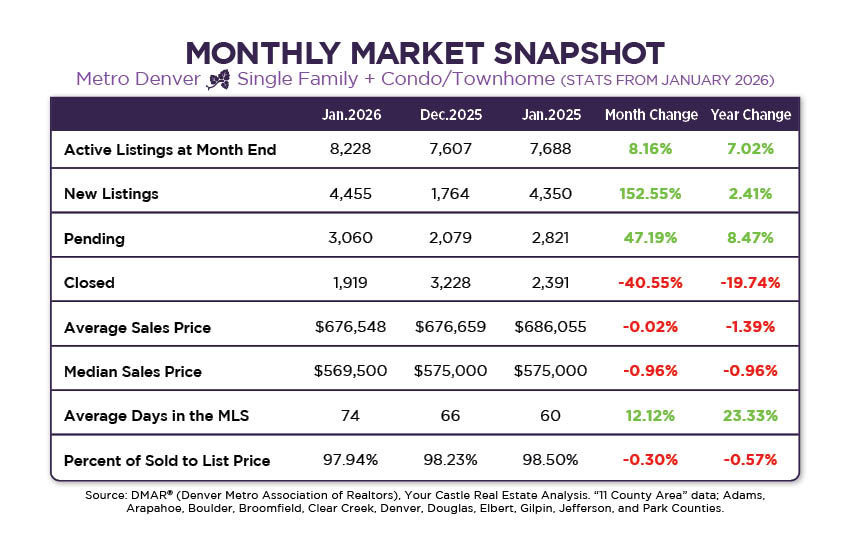

Inventory is certainly having a strong start to the year. The number of new listings in January showed a significant increase from December, coming in at 4,455 — a whopping 152% increase month over month. The number of active listings at month’s end totaled 8,228, an 8.16% increase from December. Notably, this is stronger than the historical average January change, which typically shows a 3.28% decline month over month. For context, the average number of active listings in January (1985–2025) is 11,926. The highest January on record was 2008 with 24,550 listings, while the lowest was 2022 with just 1,184 listings. This upswing in inventory may be twofold. December saw a larger-than-usual number of homes expire or withdraw from the market, and many of those sellers appear to have regrouped and re-entered in January. The unusually warm winter could also be contributing to what feels like an early start to the spring real estate season.

Both average and median days in MLS increased, with average days on market at 74, a 12% month-over-month increase, and median days in MLS at 53, a 17% month-over-month increase, reinforcing what we’ve been seeing: homes are simply taking longer to sell. Sellers are starting to adjust without panic. There’s growing recognition that today’s market requires more time and intention. Gone are the “list Thursday, under contract by Monday” norms. Instead, we’re seeing a return to thoughtful pricing, stronger preparation, and realistic expectations. Longer time on market doesn’t have to signal a lack of demand — it often means buyers are being more deliberate.

Pending sales saw a significant jump in January, likely influenced by December’s wave of expired and withdrawn listings returning to the market, along with fresh inventory hitting at the start of the year. Pending sales increased 47.19% from December, with 3,060 homes moving under contract. Because pending status is reflected almost immediately once a contract is written, this metric gives us a more real-time look at buyer activity.

Closed sales, however, tend to lag. Closings were down 40.55% in January. Unlike pending status, a property does not move to closed until the transaction is fully complete — typically about 30 days after going under contract. That means January’s dip in closed sales is largely reflective of our significantly slower holiday season. We should expect to see the influx of closings from January’s surge in activity show up in February’s data.

Average and median close prices remained relatively steady. The average close price in January was $676,548, decreasing a modest 0.02% month over month and 1.39% year over year. The median close price came in at $569,500, decreasing just under 1% both month over month and year over year, reinforcing the broader theme we’ve experienced since 2023: price stability.

For Sellers

Denver remains an expensive place to live, and buying a home continues to be challenging for many. Affordability pressures are real. If you’re considering selling, pricing realistically is critical. That means leaning on both statistical data and qualitative insight — understanding not just what sold, but why it sold.

While homes are taking longer to move, preparation still matters more than ever. First impressions are everything. Professional photography, decluttered spaces, and thoughtful presentation are the norm for desirable homes. Buyers are prioritizing affordability and practicality.

Sellers should budget for inspection-related repairs. Focus on cost-effective improvements. Avoid speculative upgrades unless they truly add value. The sellers who win in this market are the ones who prepare strategically and price precisely.

For Buyers

Inventory has improved — and that creates opportunity. However, expect bidding wars this spring on well-priced, well-prepared, well-maintained homes in strong locations. While the overall number of listings has increased, there’s still a shortage of highly desirable homes — those that are updated, reasonably priced, and located in top-tier neighborhoods.

Buyers who are financially prepared and decisive will have the greatest advantage. Hesitation on the right home can still cost you.

Inventory is improving, activity is picking up, yet pricing remains steady. Rather than waiting for dramatic change, both buyers and sellers in 2026 may find their greatest advantage comes from acting decisively when personal timing and financial readiness align.

Comments